Mar

27

A (Very) Brief History of Inflation in America

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” — Milton Friedman, Nobel Prize-winning economist

Thanks primarily to bad governmental policy, Americans have noticed their hard-earned dollars are buying noticeably less these past couple years. Certainly, many have noticed price increases in food and drink, along with household goods. Most impacted, however, are the fuel and transportation industries.

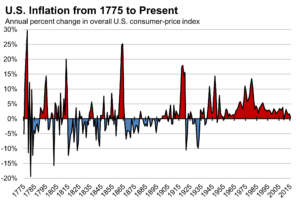

Of course, this is far from the first time that America has gone through a period of economic inflation. The specific circumstances vary, but the reasons boil down to well-known (and oft-ignored) principles. Columnist/editor/author John Steele Gordon writes on this sort of thing for a living, and he recently gave a lecture titled “Inflation in the United States” for Hillsdale College. Obviously, it was not comprehensive, yet it was packed with information. For those who don’t want to read the full adaptation of that lecture, I present a somewhat-edited version below.

— — —

“In the sixteenth century, as the gold and silver pouring into Spain from the New World caused a rapid rise in the European money supply relative to the production of goods and services, prices rose about 400 percent over the course of the century.

There was no inflation in the American colonies for the simple reason that the money supply was only a hodgepodge of foreign coins (most commonly the Spanish dollar), tobacco warehouse certificates, beaver and deer skins, wampum, and paper money printed by the colonial governments. Much trade was conducted on a barter basis.

But when the American Revolution began, both the new state governments and the Continental Congress had to find ways to finance it. Having limited ability to borrow and to lay taxes, they quickly began printing money…. [T]he so-called ‘continentals’ depreciated rapidly in value, becoming essentially worthless by the end of the Revolution….

In addition to the problem of fiat money [i.e., money that is money only because the government says so], the Continental Army forced farmers to sell their produce at whatever price the requisitioning officers chose to put on it. They were paid in quartermaster and commissary certificates, which also circulated as money at a fraction of their face value.

The need to deal effectively with the massive debts incurred in the Revolution was one of the main drivers of the Constitutional Convention that met in Philadelphia in the summer of 1787. The new Constitution and the monetary and tax systems put in place by Alexander Hamilton, the first Secretary of the Treasury, would keep inflation at bay until the great crisis of the Civil War came 75 years later….

[The United States adopted the gold standard in 1837, when it set the price of dollars at $20.66 per troy ounce of gold. This was, of course, seriously disrupted by the Civil War.] War is, by far, the most expensive of all government operations. And both the Confederate and United States governments faced unprecedented financial stresses in funding the Civil War. How each of them met the challenge helped determine, in no small degree, the outcome of the war.

Governments have only three ways to fund operations. They can tax, they can borrow, and they can print. Both governments did all three, but the particular mix was very different.”

— — —

In short, the North’s more robust economy and financial system meant that it only needed to rely on printing fiat money for about 12 percent of its revenue needs. It printed $450 million in “greenbacks”, which of course caused inflation, but it was a “manageable” 75 percent rise in prices. The South, on the other hand, relied on newly-printed money for over half of its war-time revenue — to the tune of about $1.5 billion. Plus, counterfeiting was a big problem.

— — —

“The result was catastrophic inflation. Prices rose 700 percent in the South in just the first two years of the war. As the war continued, the inflationary spiral deepened and the southern economy began to spin out of control. Living standards fell sharply while hoarding, shortages, and black markets spread, eroding popular support for the war.

With the end of the war, Confederate bonds and paper money became worthless — indeed, redemption of the bonds was explicitly forbidden by the 14th Amendment, ratified in 1868. The South, deeply impoverished by the war and dependent on agriculture and extractive industries, would be essentially a third-world country inside a first-world country well into the twentieth century….

The gold standard, where the government stands ready to buy or sell gold in unlimited quantities at a fixed price for its currency, makes inflation impossible. If the market begins to have doubts about the value of the currency, it will increasingly trade it for gold, as would foreign central banks. Consequently, the government must rein in the money supply to avoid being forced off the gold standard.

The gold standard was very popular with bankers and industrialists, as it protected the value of their assets. But it was equally unpopular with chronic debtors, such as farmers, who wanted to be able to pay back their loans with cheaper money.

Pulled in two directions, Congress — as legislatures in democratic countries often do –tried to have it both ways. It put the country fully back on the gold standard on January 1, 1879, soon after passing the Bland-Allison Act in 1878 — an act requiring the Treasury to buy on the open market between $2 million and $4 million worth of silver every month and coin it at the ratio of 16-to-1 with gold.”

— — —

An increased supply of silver dropped its market price to about 20-to-1 by 1890, but the Treasury bought most of the silver that was produced and still “coined” it at the 16-to-1 ratio. Thus, “people increasingly kept the gold and spent the silver.”

— — —

“The very large budget surpluses of the 1880s masked the government’s schizophrenic monetary policy. But when the crash of 1893 marked the onset of a new depression and government revenues plunged, the trickle of gold out of the Treasury turned into a flood. Only some very fancy footwork by the country’s leading banker, J.P. Morgan, kept the U.S. from being forced off the gold standard in 1895.” [When “sound money” William McKinley beat “pro-inflation” William Jennings Bryan in the presidential election of 1896, it kept us on the gold standard until 1933.]

The outbreak of World War I caused many disruptions in the American economy even before we entered the conflict two-and-a-half years later. With Russian grain exports blockaded, demand for American wheat soared, as did allied orders for ships, railroad rails, munitions, and other war matériel.

As a result, prices rose nearly 100 percent in the first two years of the war. When the United States entered the conflict, the federal government set up a series of boards to negotiate prices with producers to see that prices stayed in check while assuring a supply of vital materials. The Price Fixing Committee set maximum prices for such materials as coal and steel, but these maximum prices quickly became the standard prices. The only commodity that had a fixed price by statute was wheat.

With the end of the war 20 months later, the American economy soon returned to normal. Prices fell back to more modest levels, partly due to the very sharp, but short, recession of 1920-21.

The beginning of the Great Depression in 1929 brought not inflation but deflation, which can be an even bigger problem. [But, we’ll skip that, since our focus here is inflation.] …

With the onset of World War II and the U.S. becoming the “arsenal of democracy,” inflation would have quickly returned as the American economy experienced shortages in many vital commodities. But strict wage and price controls were put in place and many commodities, such as sugar, butter, red meat, shoes, and gasoline, were severely rationed. Some commodities in particularly short supply, such as rubber and building materials, simply vanished from the marketplace.

But while the wage and price controls kept wartime inflation down to about 25 percent, they did not eliminate the inflationary pressures — they only postponed them. When President Truman ended wage and price controls at the beginning of 1946, inflation came roaring to life. The U.S. experienced the greatest peacetime inflation up to that point, as non-governmental spending rose by 40 percent. But the supply of goods could not expand nearly as quickly, as industry needed time to switch over to peacetime production….

[A number of factors — which I will not get into here — kept the economy from returning to a post-war depression.] By the late 1940s, with the government usually running modest budgetary surpluses and industry once again on a peacetime footing, inflation subsided and the economy grew quickly, doubling between the end of the war and the mid-1960s.

But it was not to last. When Lyndon Johnson acceded to the presidency on the death of John F. Kennedy, he wanted to complete the New Deal. He pushed through a number of programs, including Medicare and Medicaid, Head Start, and the Mass Transit Act. These new programs caused a breathtaking rise in non-defense federal expenditures. Between 1965 and 1968, they rose by a third, from $75 billion to $100 billion. Because of the Vietnam War, military expenses went up as well, from $50 billion to $82 billion.

This new spending inevitably caused an increase in inflation, which had been minimal since the immediate post-war years. A vicious cycle developed, with lenders demanding higher interest rates to protect them from inflation, while the Federal Reserve pumped up the money supply by buying federal bonds to keep interest rates down.

[Congress passed a bill in 1974 that removed the President from the budgetary process, and soon spending was out of control.] By 1980, the inflation rate hit 13.5 percent, the highest peacetime rate in history. Although the national debt increased by two-and-a-half times in the 1970s, so great was the inflation in that decade that the debt actually declined as a percentage of GDP.

Only when Paul Volcker became chairman of the Federal Reserve in 1979, and Ronald Reagan became president in 1981, did inflation end. The Federal Reserve sharply increased interest rates, pushing the economy into a deep recession. Unemployment hit 10.8 percent at its peak, the highest since the 1930s. But it worked. Inflation, which had been 13.5 percent in 1980, was down to 4.1 percent in 1984 and would stay low for the next few decades.

When the economy went into a deep recession with the bursting of the housing bubble in 2008, however, the government began running unprecedented budget deficits. The national debt, over $10 trillion in 2010, would double by 2017. With the onset of the COVID pandemic in 2020, deficits soared further as the government sought to mitigate the effects of shutting down much of the economy. The national debt now stands at $29 trillion — about where it was in 1945, relative to GDP.

But this breathtaking increase in the money supply did not, at least immediately, set off inflation. For while inflation is a monetary phenomenon, it is also a psychological one: when the expectation of inflation becomes widespread, it becomes a self-fulfilling prophecy.

That prophecy was fulfilled in 2021. With the Biden administration continuing pandemic relief, which discouraged many from seeking work, and restricting oil and gas production, inflation set in. Supply chain disruptions also contributed.

By December 2021, consumer prices were up seven percent on an annual basis, the highest in 40 years, while producer prices were up 9.6 percent, the highest since that statistic has been compiled. And the expectation of further inflation is now deeply embedded in the economy.”

— — —

And, that brings us to today….

Yet, still the Biden/Harris administration and its compatriots in Congress and elsewhere push to add another $5 trillion or more to the national debt with the “Build Back Better” plan. Add in things like the threat to Ukraine — i.e., “the world’s bread basket” — and we can plan on years more of inflation. The only thing we citizens can do is continue to make our voices heard and make sure there is a huge Red Wave in the 2022 elections and beyond.

Also, I’m certainly no expert, but we should really consider going back to a gold-based or bimetallic currency.

* Portions of this article have been adapted or “Reprinted by permission from Imprimis, a publication of Hillsdale College.”